Perpetual Futures-Spot Arbitrage sounds like science fiction. But nothing about Star Trek and Captain Spot! (or was his name Spock? 🤔) Behind the term lies merely a clever trading strategy. With cryptocurrencies a new type of futures contracts has emerged: Perpetual futures. These are futures that do not have a delivery date. Of course, there is also a chance to profit from its difference to the spot market. In arbitrage trading with perpetual futures you have the opportunity to earn the funding rate of 0.01% interest (and more) every 8 hours. As with almost all arbitrage trading strategies, the risk is low and the application is relatively simple. Learn how to apply the strategy concretely on Binance in this article.

In my article Contango: Your Chance for a Low-Risk Profit I have already described how to arbitrage the gap between the spot and futures market with delivery date. In contrast to this trading strategy, arbitrage trading with perpetual futures is not about profiting from the gap between the markets. You arbitrage them in other ways. However, in order to understand the differences between the two trading strategies, let’s compare the relation of the two futures markets with the spot price.

Delivery futures vs. perpetual futures

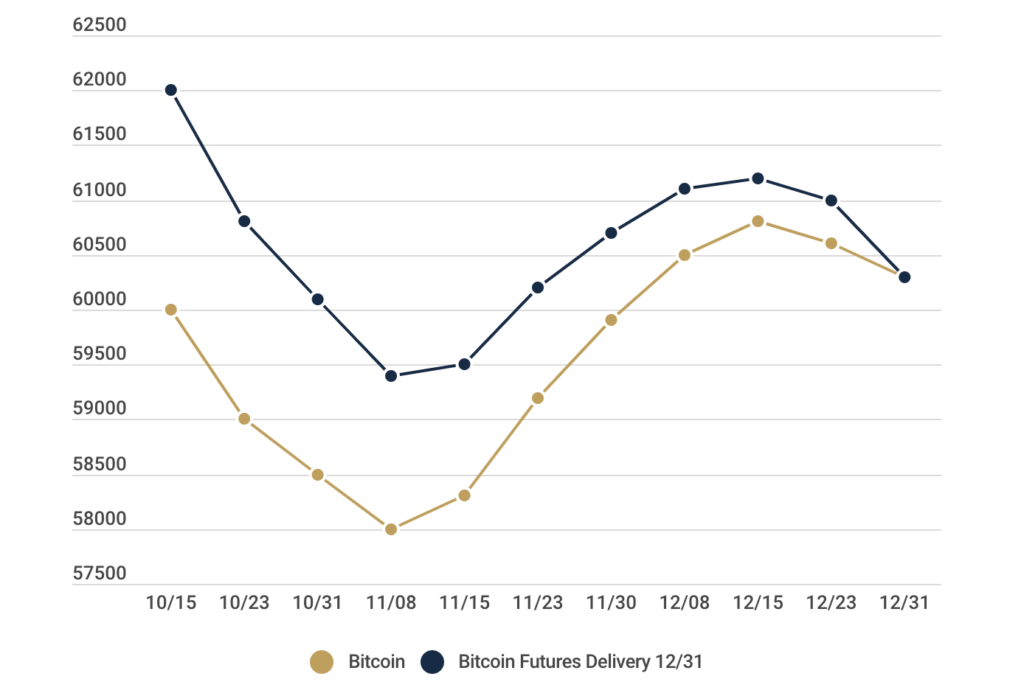

Futures are always traded higher in the bull market than the underlying asset. I have already described the reasons for this in detail in my article about contango. To recall the correlation of spot and futures market, let’s look at the following chart.

As can be seen in the chart, spot and futures market with delivery date inevitably converge and meet at the delivery date.

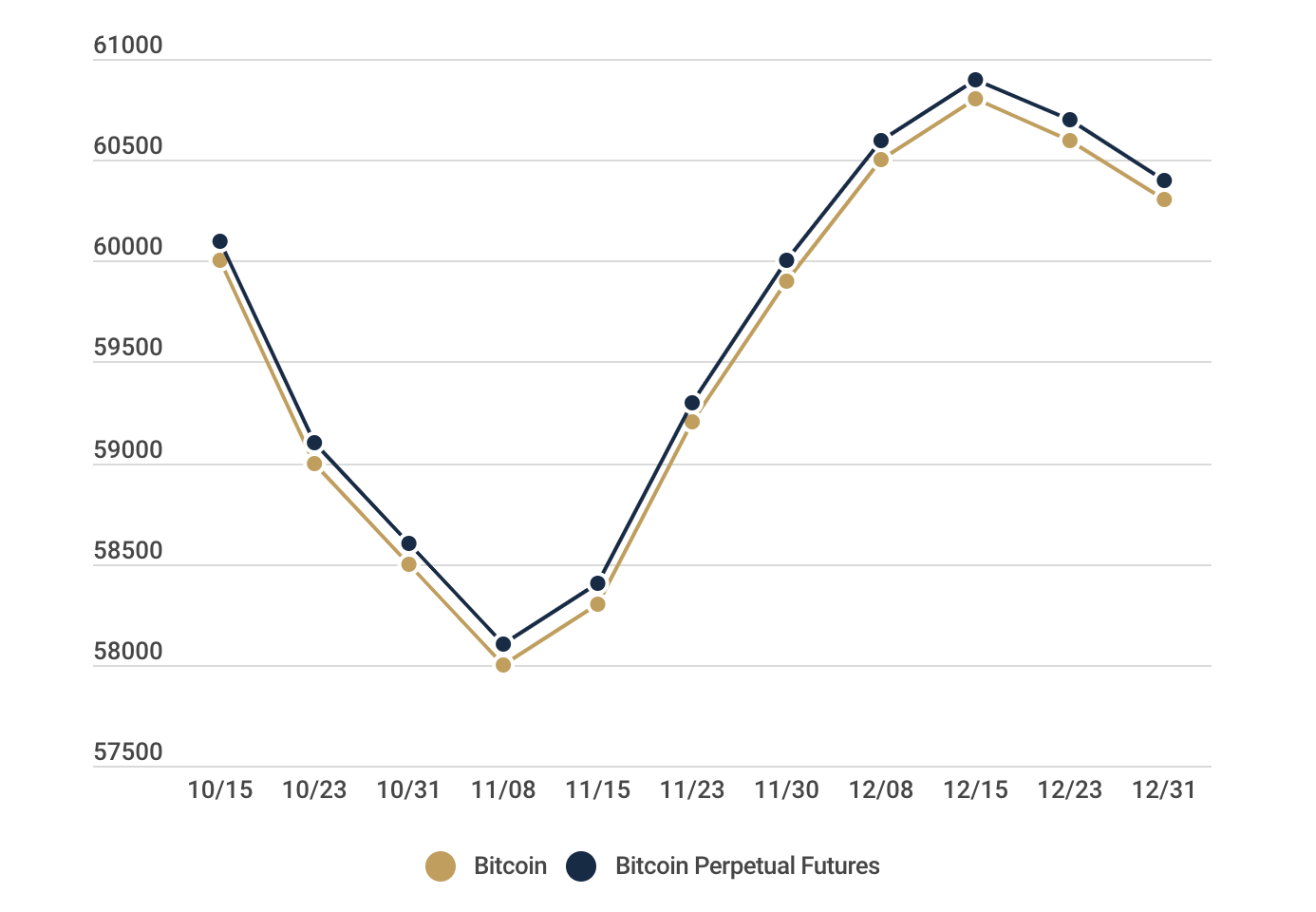

With perpetual futures, the situation is different. Since they do not have a delivery date, the spot and futures markets never meet. In a bull market, investors therefore always assume that the price of the underlying asset will rise. In bearish times, it is the other way around. The following chart shows an example development of spot and perpetual futures price in the bull market.

Unlike futures with a delivery date, the futures price in a bull market is always only slightly higher than the spot price. Since the two prices never converge, the opportunity in perpetual futures spot arbitrage has to lie somewhere else than in cash and carry. It lies in the so-called funding rate.

Funding Rate: the basis of arbitrage trading with perpetual futures

In standard futures transactions, the delivery date ensures that the futures price is not driven up excessively. The further away the delivery date is, the greater the difference to the spot price in the bull market. Over time, the futures price moves closer and closer to the spot price because the delivery date is also getting closer.

Perpetual futures have no delivery date and the underlying asset is consequently never traded. In mathematical terms, the delivery therefore would take place in the infinite future. If we now apply the logic from futures with delivery to perpetual futures, the price of the futures would also have to be enormously high if the delivery date is in the infinite future, right? The more optimistic investors are, the greater the difference would be.

To prevent this, the funding rate was introduced.

The eternal laws of futures trading

In order for you to understand the funding rate, it is fundamental to recall the following facts about futures trading.

- Futures are traded with long and short positions. Short Selling? Long Buying? Finally a Simple Explanation

- When investors are optimistic, they buy futures (long position).

- Investors expecting a falling price go short with futures.

- In the bull market, more investors buy futures and fewer investors short them.

- The more investors buy futures, the higher its price rises.

The Funding Rate adds the following conditions to the set of rules.

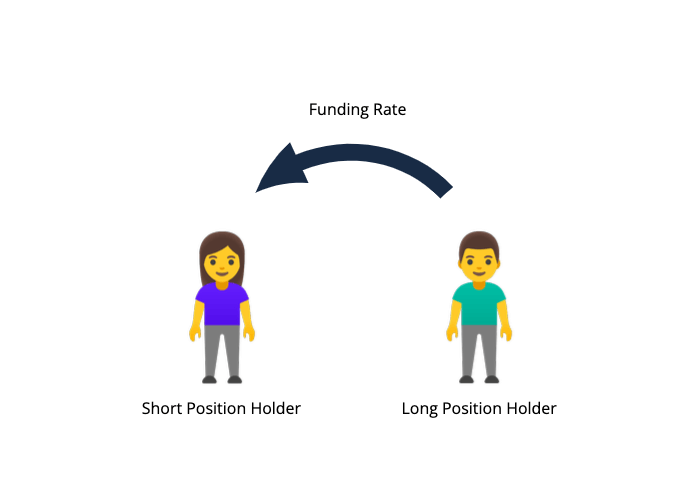

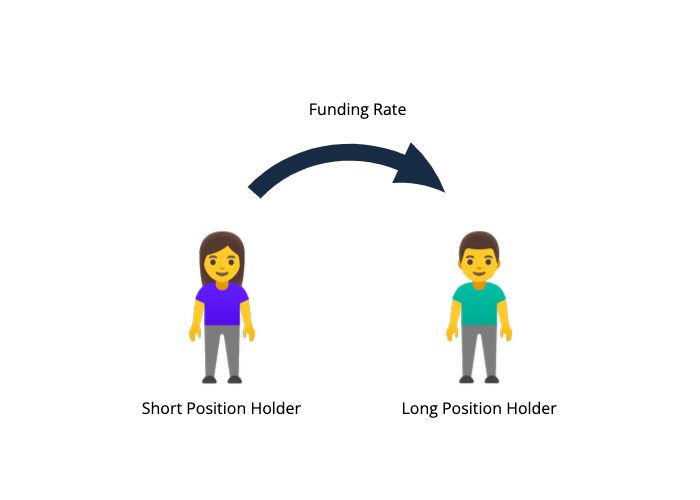

- If the futures price is higher than the spot price, then holders of futures (long position) must pay a fee.

- If the spot price is higher than the futures price, then holders of futures short positions must pay a fee.

- The funding rate is not paid to the broker. The broker only transfers it between holders of short and long positions. For example, if there are more holders of futures, then the broker charges them the fee and transfers it to the holders of short positions.

- The fee accrues every 8 hours.

- Usually, the funding rate is 0.01% of the traded volume. If the imbalance of spot and futures price increases, then the fee also increases.

The funding rate in the bull market

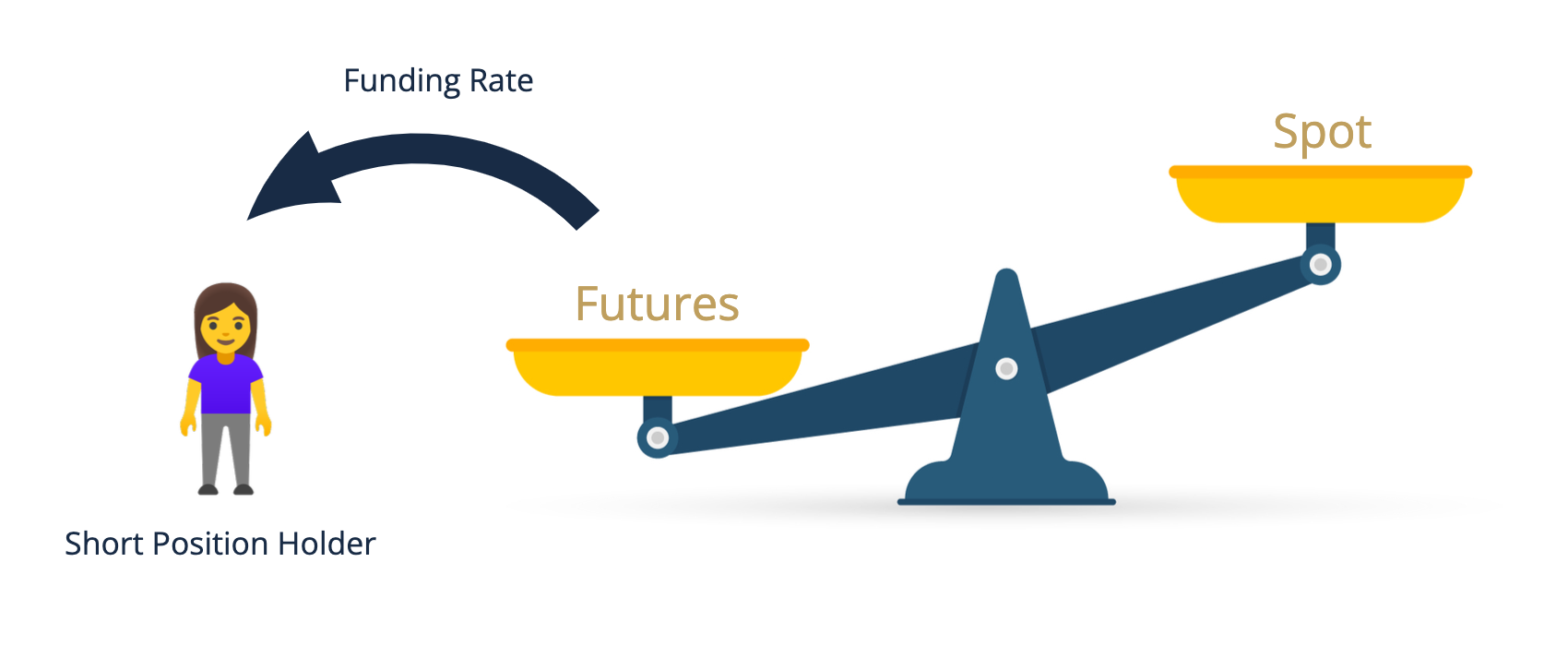

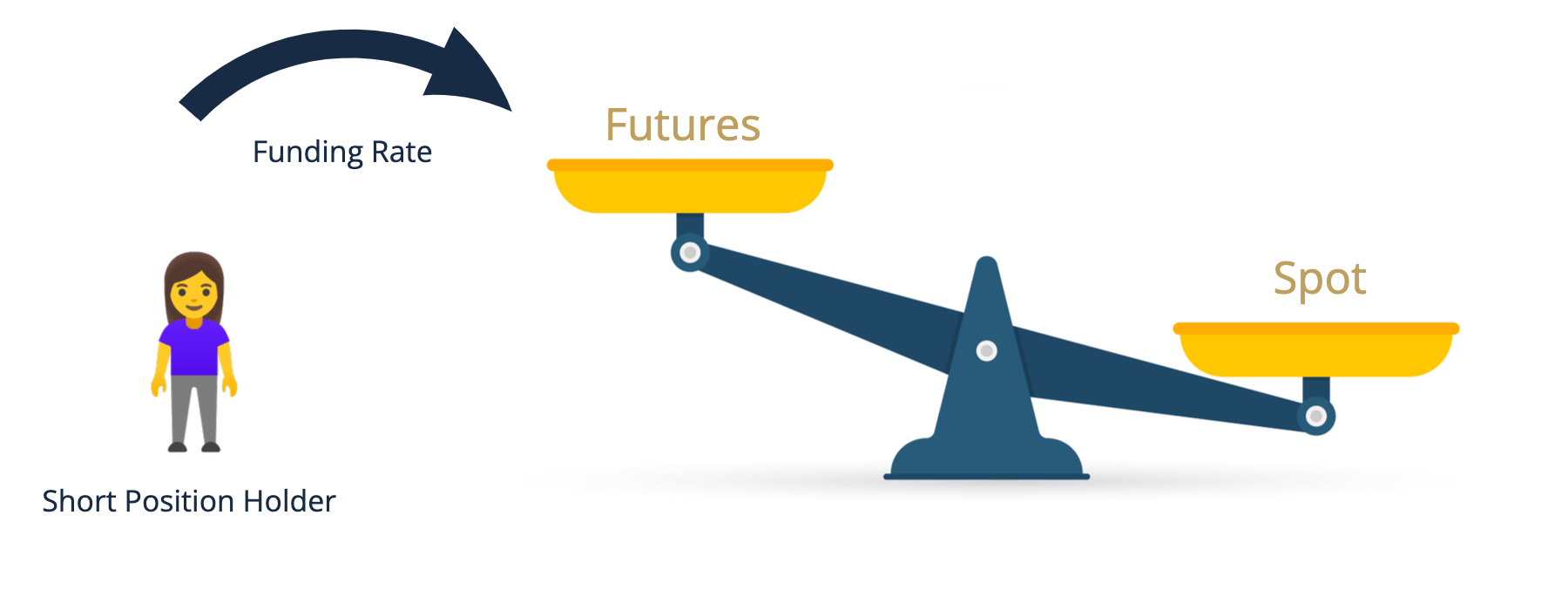

In a bull market, more investors buy futures, which pushes the price upwards. The imbalance to the spot market is often illustrated in the sense of a scale: the more investors buy and hold futures, the heavier the weight of the futures side becomes. In comparison, the side of the spot price weighs thus much lighter.

To restore balance, the broker has to take «weight» away from the invested volume. This load in the form of the funding rate is transferred by the broker to the holders of short positions.

More precisely, the holder of short positions does not receive the fee directly from the broker, but from investors who hold long positions.

This measure has various effects:

- Less volume in holding futures means that the price of futures decreases.

- More volume in holding short positions means that the futures price decreases.

- The higher the funding rate, the fewer investors buy futures.

The funding rate in the bull market is the chance for your free money. But more about that later.

The funding rate in the bear market

For as long as I have known cryptocurrencies and especially Bitcoin, buyers of futures have been obligated to pay the funding rate. As we all know, times are not always bright and the wind will turn. Then, when more investors become pessimistic and assume that the price of an asset will drop, they will thus open more short positions in the futures market. This leads to a relatively low futures price compared to the spot price.

If we apply the analogy of the scales here again, this means that there is too little weight on the futures side. In this case, the holders of short positions are in charge.

And here as well, the fee is transferred directly between the investors.

In addition, this change in cash flow also causes a change of effects.

- Less volume in holding short positions means that the price of futures increases.

- More volume in holding futures means that the futures price increases.

- The higher the funding rate for holders of short positions, the fewer investors short futures.

«Now I finally want to know how to collect the funding rate!»

Okay okay not so fast! The basics are really important. And with the knowledge from above combined with a pinch of know how from abitrage trading with contango we cooked the delicious dish: 0.01% profit every 8 hours. And it goes like this.

You buy Bitcoin, transfer them to the futures wallet and short the same amount of Bitcoin futures. As collateral you deposit the bitcoin you bought before. You are in a neutral position. Let’s quote my post about contango:

And if you now know how to get into the neutral position, then you can stay in this position. And in addition, investors who hold long positions pay you the funding rate every 8 hours 💰. If the funding rate is 0.01% per 8 hours, this corresponds to a return of 0.03% per day and 10.95% per year!

Hands-on: Funding rate as passive income on Binance

The following instructions should help you to apply the strategy yourself. Since I am primarily on Binance, the screenshots were taken therefore on this trading platform.

Create your account on Binance here and get 10% discount on all trading fees.

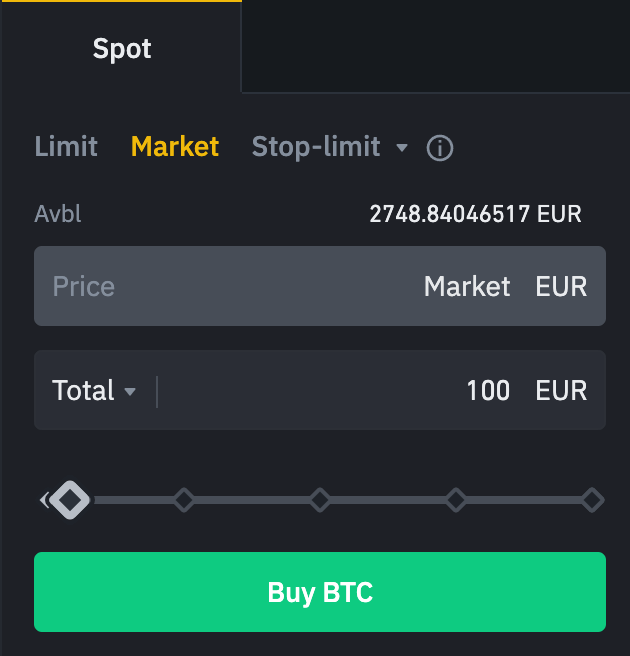

1. Purchase of BTC in the spot market and transfer to the futures wallet

You are probably already used to buying cryptocurrencies in the spot market. The following screenshot shows you the purchase of Bitcoin for €100 at the current spot market value.

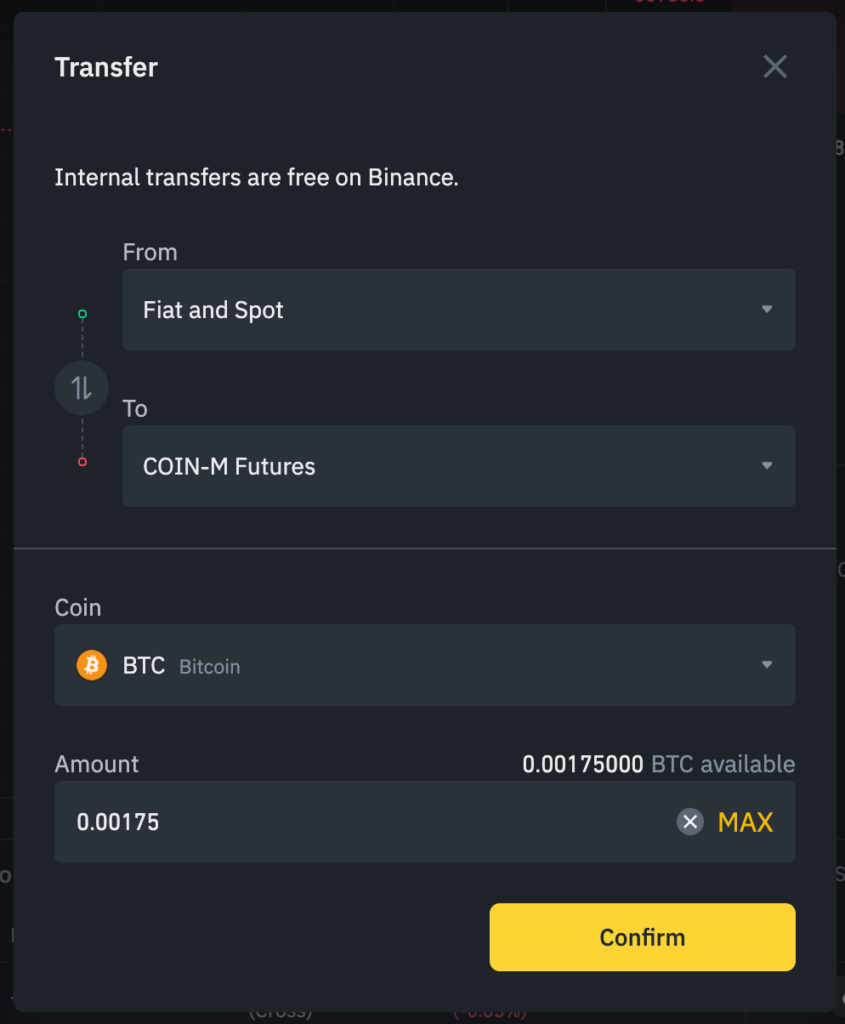

In order for you to get into the neutral position and collect the funding rate, you need to deposit a collateral. The BTC you just bought is supposed to be this collateral and therefore, now switch to Binance Futures -> Coin M Perpetual. Via the button «Transfer» and the popup that opens, you can transfer the purchased BTC from your spot wallet to the futures wallet.

As with the cash and carry trading strategy, it is advisable to complete these steps quickly. Because until you have opened your short position in the futures market, you are exposed to the fluctuations of the market.

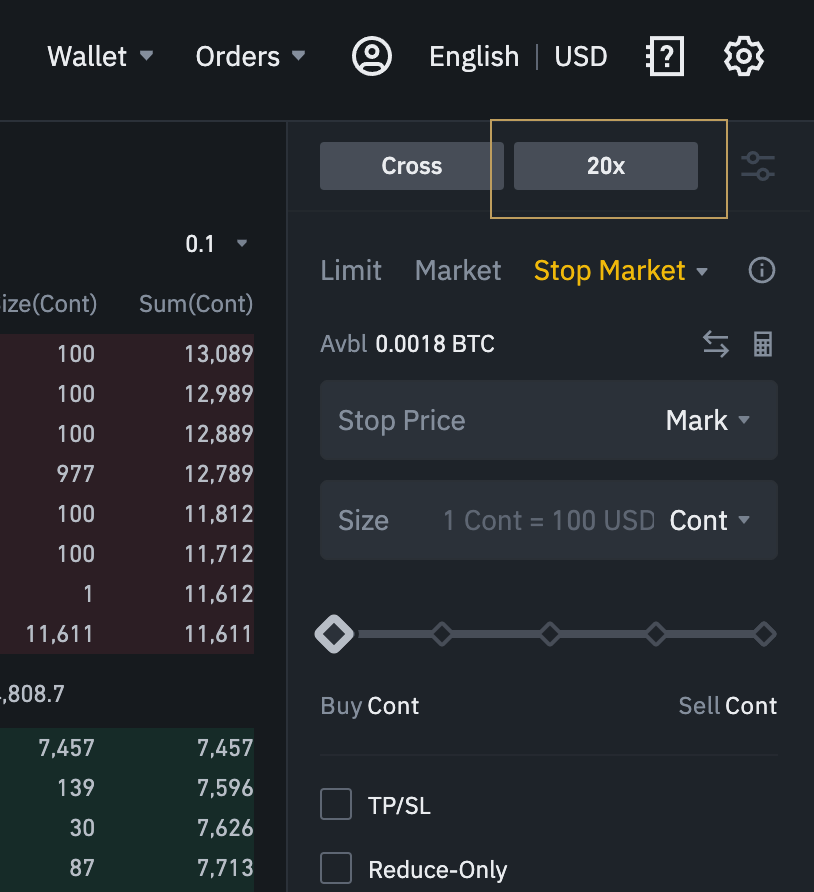

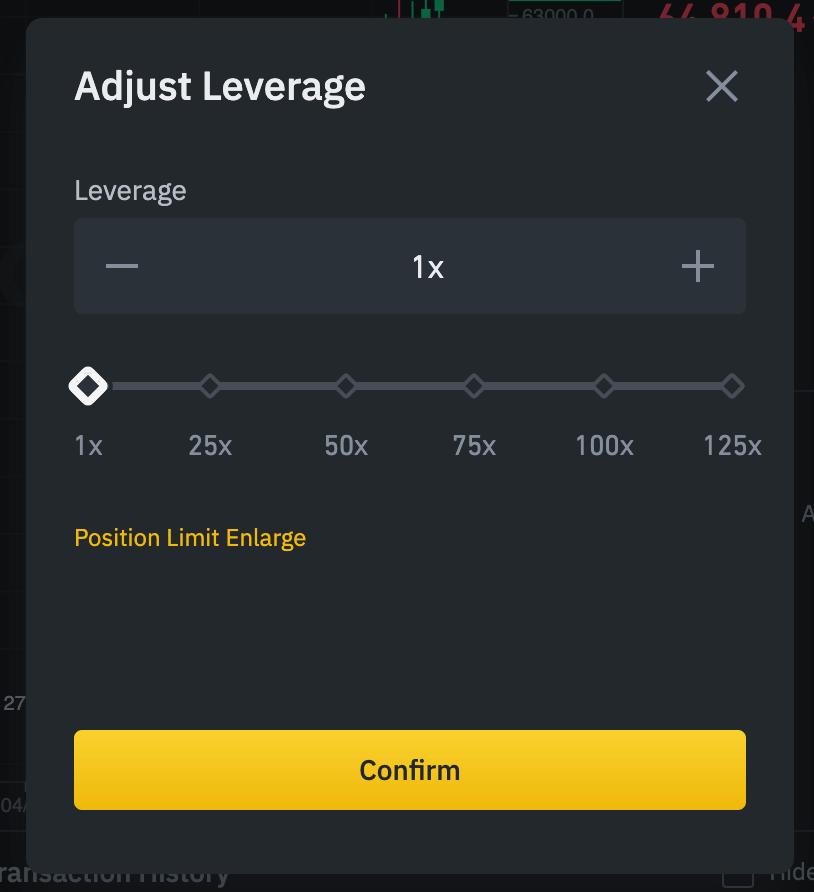

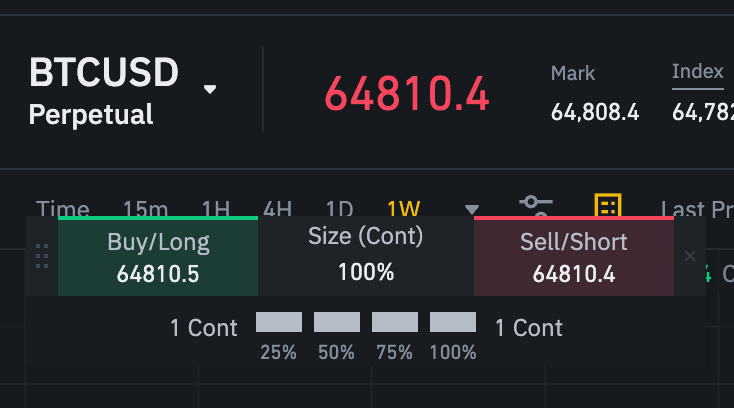

2. Adjust leverage and open futures short position

In order to use the arbitrage trading strategy with low risk, it is important that you first lower the leverage of your shorted futures.

Confirm the 1x leverage with «Confirm» and look at the form which overlays the graph. There you select «100%» and click on «Sell/Short».

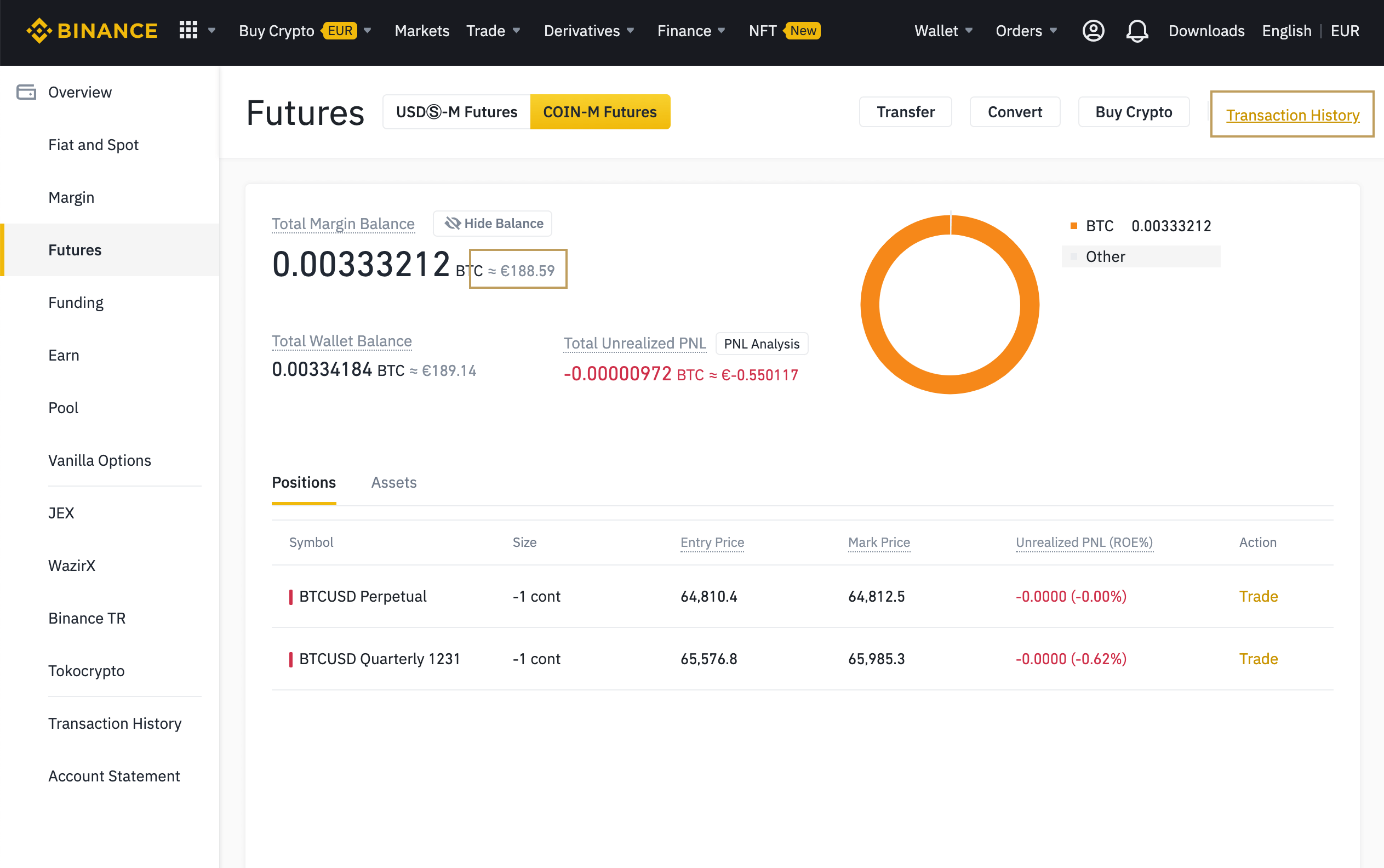

3. Monitor return on investment

After placing the short position, it is recommended to take a look at the futures wallet every now and then. In my example, the total amount is more than the previously purchased BTC for 100€. The reason for this is just more open futures positions.

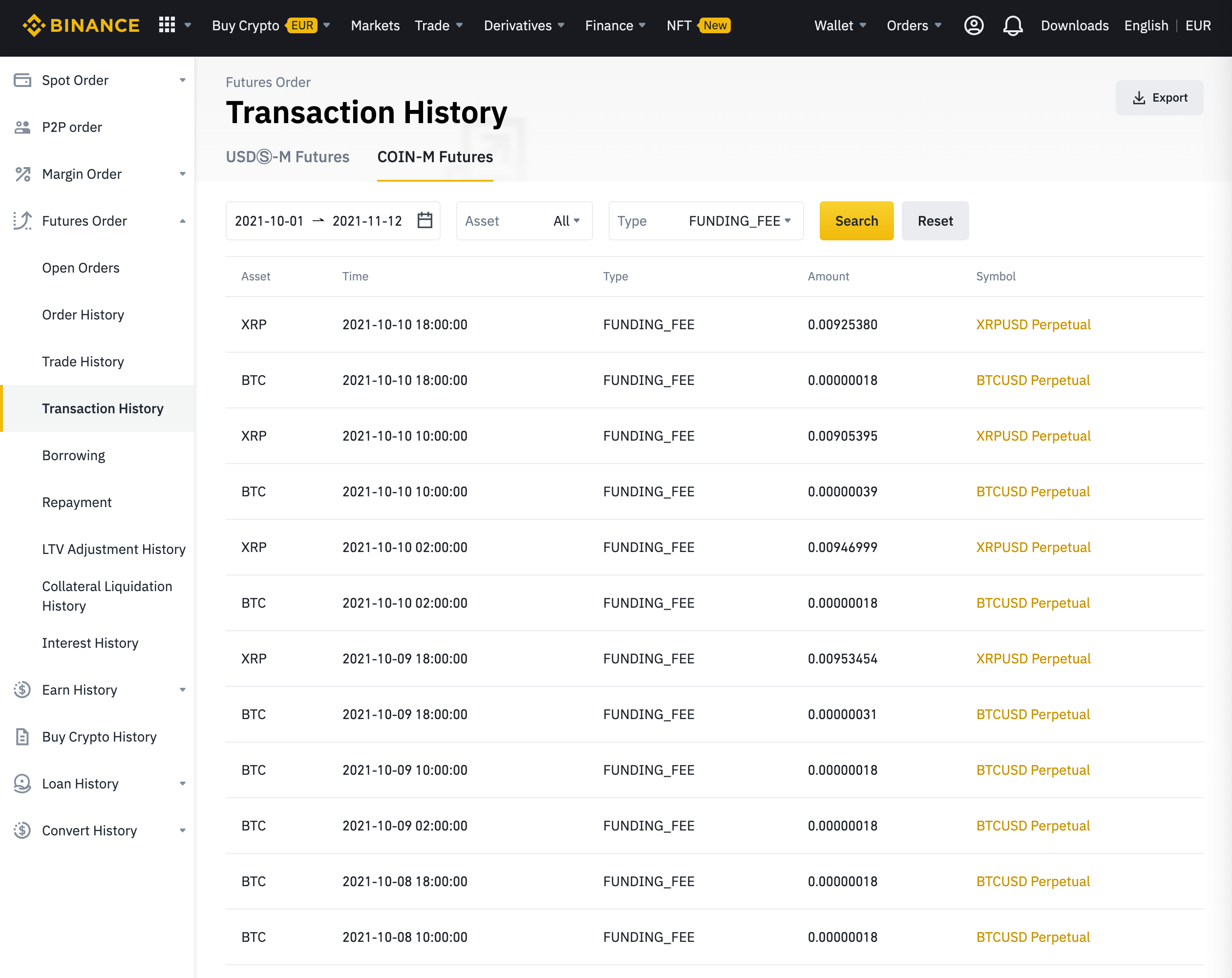

The golden framed value should be equal or higher than your invested capital at any time. Since you are in the neutral position, «Total Unrealized PNL» and «Total Wallet Balance» always balance out. By clicking the «Transaction History» button you can view the received funding rate amounts over time.

My screenshot shows additional entries for the funding rate of XRP (Ripple). I have already tried the trading strategy with a wide variety of cryptocurrencies and, thus, you are not bound to Bitcoin.

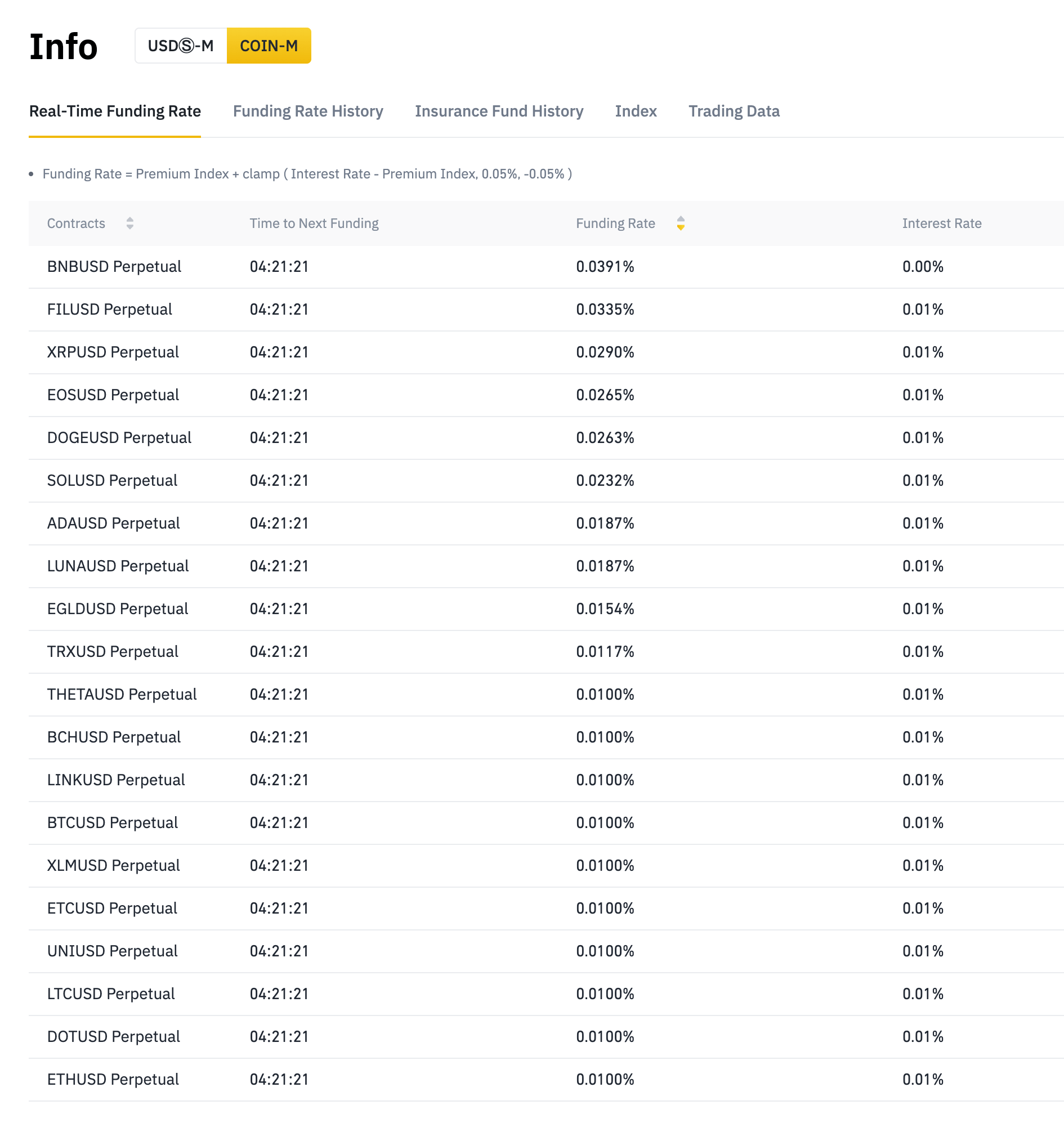

List of latest funding rates

On Binance you can always check the current funding rates: https://www.binance.com/en/futures/funding-history/0

Every now and then I take a look to see which cryptocurrency is yielding the most based on its current rate.

The highest rate at the time of the screenshot is 0.0391%. This corresponds to a potential annual return of 43% (0.0391% * 3 * 365) with when taking advantage of the funding rate. However, to maintain this annual return, the funding rate for the BNBUSD futures market would have to remain permanently at that high level. This case is basically impossible. In the screenshot above, the BNB Coin just experienced a temporary high.

It is recommended not to switch too often between the different currencies when using the arbitrage trading strategy. When trading in the spot and futures market, fees are incurred, which you must first earn again via the funding rate to make a profit. In addition, the rates can change very quickly. However, you can expect a minimum return of 0.01% per 8 hours in a bull market.

So what’s the next step?

The trading strategy is very exciting, profitable and does not involve big risks. To answer the question in the title, yes, the funding rate is free money if you apply the trading strategy correctly. However, cryptocurrencies wouldn’t be innovative if applying them wasn’t even easier. Meanwhile, there are bots that execute the arbitrage strategy completely on their own for you. The only thing you need to do is transfer USDT, choose a currency and lean back. The post about it will follow… See you then! 💰📖